Ivy League Endowments 2016 Performance Review

An 1873 meeting that brought Harvard, Yale and Princeton together to codify the rules of American football also debuted a sports conference later known as the “Ivy League -- eight elite institutions whose heritage, dating from pre-Revolutionary times, became formative influences shaping American character and culture. These schools also pioneered endowment investment management, thus helping to secure the nation’s educational legacy for posterity.

An 1873 meeting that brought Harvard, Yale and Princeton together to codify the rules of American football also debuted a sports conference later known as the “Ivy League — eight elite institutions whose heritage, dating from pre-Revolutionary times, became formative influences shaping American character and culture. These schools also pioneered endowment investment management, thus helping to secure the nation’s educational legacy for posterity.

An 1873 meeting that brought Harvard, Yale and Princeton together to codify the rules of American football also debuted a sports conference later known as the “Ivy League — eight elite institutions whose heritage, dating from pre-Revolutionary times, became formative influences shaping American character and culture. These schools also pioneered endowment investment management, thus helping to secure the nation’s educational legacy for posterity.

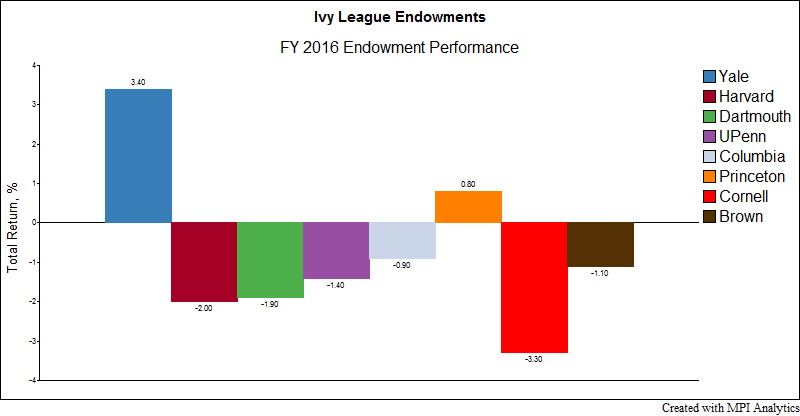

Yale’s unprecedented domination of the 2016 intra-mural contest over endowment investment returns bears all the earmarks of an autumn classic. The performance is all the more noteworthy when contrasted with that of arch-rival Harvard’s endowment, whose disappointing $2 billion drop in value is likely to both limit funding for University programming and, noted President Drew Faust, prompt a reconsideration of Harvard Management Company’s entire investment strategy.

Based on our endowment study last year, we decided to take a closer look at Ivy League endowment performance in 2016.

Sign in or register to get full access to all MPI research, comment on posts and read other community member commentary.

Trusted by